2025 Consulting Market Overview

A glance at market trends in consulting in 2025...

- Consulting is not slowing, it's adapting to meet new expectations

- Equity, incentives & the changing compensation model in consulting

- Private Equity (PE) activity remains resilient, but has the game changed?

- Life Science consultancies expand beyond Strategy & Market Access in a cautious hiring climate

- How talent intelligence is powering global expansion

- Case Study: Expansion in the GCC and SEA markets

- Market Summary

Consulting is not slowing down, it’s adapting to meet new expectations

Changing Client Priorities

This year, businesses have become noticeably more selective and risk-conscious, favouring consulting partners that can deliver clear, measurable financial results over those focused solely on pure strategic or exploratory R&D.

The shift is especially evident in the Life Sciences sector, where rising regulatory scrutiny, complex supply chains, and operational inefficiencies have fuelled a sharp rise in demand for process-driven consulting engagements. Firms delivering integrated, outcomes-led solutions that extend beyond pureplay strategy are maintaining momentum – scaling both efficiently while maintaining a competitive market edge.

Despite concerns about market stagnation, consulting isn’t slowing down, it’s evolving.

How are consultancies adapting?

- Value-based pricing is becoming more common, with fees tied directly to measurable client outcomes. This is increasing transparency and strengthening long-term trust with clients.

- Integrated delivery models are on the rise, with consultancies embedding cross-functional teams within client organisations. Many are ramping up on hiring client services teams to win larger MSAs and maintain delivery capacity across new and existing accounts.

- Firms are expanding across sectors and capabilities. This has been demonstrated across Financial Services, Industrials, and Energy sectors. Demand for Strategy & M&A support through to large-scale transformation programmes is driving stronger project pipelines.

- Growing investment in talent intelligence is helping firms make better strategic decisions, even in periods of limited growth or hiring activity.

“This year, we have seen several trends unfold. There is significant investment in strategic growth initiatives as firms develop new service pillars and expand existing offerings beyond pure strategy. Consulting clients are focused on adding critical mass through acquisitions and targeted team hires, while boutiques continue to grow organically despite ongoing capacity constraints. Competition for talent is intensifying, with firms adopting creative talent strategies to differentiate through stronger value propositions and more competitive compensation packages.” - Kerone Daniel, Managing Director

Equity, incentives & the changing compensation model

Traditional partnership models are out of step in today’s consulting market. High-growth firms are increasingly moving toward performance-driven, incentive-led compensation structures, with a marked increase in the use of long-term incentives this year.

While competitive base salaries still matter, top-tier talent is placing greater value on meaningful ownership tied directly to company growth. High-performing leaders want rewards linked to impact rather than tenure, alongside clear line of sight to long-term financial upside. In response, many PE-backed consulting firms are extending equity participation even beyond Partner level talent. Tools such as phantom shares, RSUs, and profit-sharing have enabled many firms to deliver ownership-like benefits without the rigidity of traditional partnership models – strengthening retention, accountability, and firm-wide growth.

Successful firms are striking the balance between financial incentives and creating a culture of empowerment, ensuring that performance, ownership, and strategic alignment work together to build long-term value for the business.

Currently, 58% of consultancies offer long-term incentive rewards as part of their compensation package. These are delivered through genuine equity (34%), phantom shares (45%), RSUs (14%), and profit-sharing schemes (7%).

Implications to consider

- LTIs are increasingly viewed by senior-level consultants as a core component of an attractive move, not a “nice to have.”

- Firms without LTIs often risk being deprioritised by senior candidates in favour of competitors offering even modest value-sharing mechanisms.

- Traditional compensation packages may no longer be sufficient to attract senior talent; firms may need to redesign incentive structures to include ownership pathways.

- Large, traditional firms have faced difficulty in retaining senior talent, as those driven towards ownership structures will gravitate toward boutiques, PE-backed firms, and scale-ups where equity is meaningful.

Private equity remains resilient, but has the game changed?

Private equity remains resilient in 2025, but investor focus has shifted toward maximising value within existing portfolios, driving greater reliance on due diligence, targeted growth strategies and operational transformation. As a result, operational, financial and commercial due diligence are now more deeply integrated into broader investment decision-making and ongoing value-creation initiatives.

This shift is clearly reflected in hiring patterns.

Demand for private equity and M&A–related roles have seen a significant increase, with consulting firms actively expanding teams across strategy, transactions and diligence. Across industries, Strategy & M&A accounted for 79% of hires this year, with 67% focused on growth strategy and due diligence.

Our recent Partner Moves series underscores this momentum, highlighting a sustained rise in senior and Partner-level appointments across global consultancies as firms continue to invest in senior leadership to support growing demand in the private equity consulting sector.

Beyond individual hires, the broader market response is evident in how consulting firms are expanding and formalising their private equity capabilities. Leading consulting firms are scaling their transactions advisory and private equity platforms to meet growing demand, with notable examples including:

- EY-Parthenon, which has fully integrated EY’s Strategy & Transactions business to strengthen its end-to-end deal and value creation offering.

- Alvarez & Marsal, which continues to scale its transaction advisory and performance improvement teams to meet growing transaction complexity, and;

- Stax, a leading player in commercial due diligence and value creation, which announced plans to double headcount by 2025.

Life Sciences consultancies expand beyond Strategy & Market Access in a cautious hiring climate

Life Sciences consultancies are undergoing a notable shift, expanding beyond their traditional focus on Strategy and Market Access. While overall hiring remains cautious, the past year has seen a clear broadening of opportunities across our client base, driven by growing demand for integrated, end-to-end solutions across the full Life Sciences value chain.

As a result, hiring strategies are being redefined.

Demand is increasing for talent across operations, supply chain, regulatory affairs, medical affairs and digital enablement –reflecting an industry-wide push toward operational efficiency and more holistic delivery models. This marks a clear move away from purely strategic advisory toward capabilities that combine insight with execution.

The market remains sensitive, and the bar for entry has risen considerably.

Despite a 95% increase in open roles over the past year, talent mobility has remained subdued, with candidates increasingly cautious about moving in an uncertain climate. At the same time, heightened client expectations are placing greater pressure on consultancies to hire individuals who can deliver immediate impact.

In response, firms have become more selective in their hiring. Academic pedigree, GPA performance and a demonstrable, transferable book of business are carrying increased weight, as consultancies prioritise candidates who are client-ready and able to add value from day one. Rather than pursuing broad headcount growth, many organisations are choosing to remain lean – stretching existing capacity and focusing investment on high-impact, high-performing teams.

Across the market, this has translated into a preference for smaller, more experienced teams over wider resourcing models. Underutilisation and onboarding friction are no longer acceptable trade-offs, and new hires are expected to contribute meaningfully from the outset, operating with a level of maturity and independence aligned to the pace and demands of the consulting environment.

How talent intelligence is powering global expansion and hiring decisions

Southeast Asia and the Middle East are emerging as priority growth markets for consulting firms, driven by large-scale transformation programmes, rising investment and long-term national development agendas. Key opportunities span public-sector reform, digital and technology enablement, energy transition, healthcare modernisation and major infrastructure projects.

While the opportunity is significant, success in these regions requires more than market entry alone. It demands immediate local credibility. Firms must navigate language, cultural and operating differences, while competing for scarce talent that combines technical expertise with genuine regional insight.

Without strong, locally embedded teams, firms risk prolonged hiring cycles, misaligned client expectations, and operational inefficiencies. Overreliance on expatriates or remote leadership often leads to cultural disconnects, slower decision-making, and weakened delivery performance.

Consultancies are increasingly using talent intelligence to inform hiring decisions as they expand into new geographies. Used effectively, it enables firms to:

Accurately assess the local talent landscape, including availability, capability depth, and experience levels, ensuring hiring efforts are focused where they deliver greatest impact.

- Map competitor teams and market dynamics, uncovering realistic and strategically aligned talent sourcing opportunities.

- Design data-driven recruitment strategies, informed by region-specific needs, compensation benchmarks and candidate expectations.

- Navigate cultural and regional nuances that influence talent attraction, engagement and long-term retention.

- Reduce hiring and execution risk, through insight into mobility trends, retention challenges and workforce stability across local markets.

In an environment where speed, credibility and cultural alignment determine competitive advantage, talent intelligence is becoming indispensable for firms looking to scale globally with confidence.

Case Study: Global consulting firm expands in the GCC and SEA markets

Background

KRS supported a global strategy consulting firm as it expanded its local operations across the GCC and Southeast Asia. Success in both regions depended on building teams with deep regional expertise and strong local credibility to meet the needs of clients on the ground. Rather than pursuing rapid hiring, the firm adopted a strategic, insight-led approach — seeking a clear understanding of local talent availability, competitor activity and regional market dynamics before making key recruitment decisions.

Our Approach

- Talent pool mapping: Analysed key market players, market size, and candidate mobility across geographies.

- Competitor Intelligence: In-depth assessment of 5 direct competitors, benchmarking compensation bands, talent pools and value propositions.

- Localised Hiring Strategy: Developed a region-specific recruitment roadmap aligned with business priorities. Co-created a compelling talent value proposition tailored to cultural and market nuances. Collaborated closely with local leaders to customise hiring narratives.

Outcome

Within eight months, we supported the successful hiring of 13 professionals across Associate to Partner levels in Southeast Asia and the Middle East. This enabled the firm to establish a credible local presence, strengthen client engagement and accelerate its broader global expansion strategy.

By grounding hiring decisions in real-time insight into local talent markets and competitor dynamics, this firm built credible, high-performing teams faster, turning geographic expansion into a strategic advantage rather than an execution risk.

Market Summary

- Consulting demand is shifting toward value-driven, outcome-focused engagements with clear financial returns, rather than exploratory or pure strategic work.

- Life Sciences consultancies are accelerating investment in operationally focused capabilities. As firms transition toward integrated, end-to-end solutions, the demand for supply chain, procurement, and regulatory services has more than doubled.

- Firms are adopting more agile delivery models and strategic partnerships to enhance responsiveness, flexibility, and innovation in client engagements.

- Compensation models are evolving to attract and retain top talent, with formal equity and equity-like incentives increasingly extending beyond the Partner level.

- Hiring remains selective, with firms prioritising client-ready talent capable of delivering immediate impact rather than pursuing broader headcount growth.

- Talent intelligence has become mission-critical to growth and global expansion strategies, where firms must navigate local market dynamics, competitor activity and competition for skilled regional professionals.

“In an increasingly complex and cost-conscious environment, talent intelligence has become a defining driver of sustainable growth for consultancies. Firms that align hiring decisions with real-time market intelligence will build a clear competitive advantage that enables them to adapt, differentiate, and grow.” - Buse Demirbag, Head of Talent Consulting

Diving into our data...

- Hiring demand across Life Sciences

- Hiring demand across all Industries

- Top five skillsets in-demand

- Growth plans in 2026

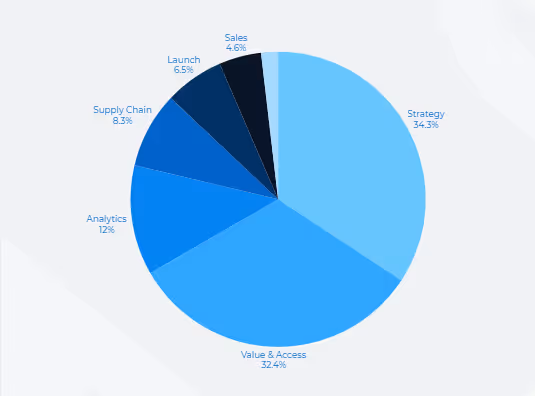

Hiring demand across core functional domains in Life Sciences

Strategy

Strategy continues to be a core growth engine, representing 34% of all client mandates. Demand is being fuelled by the need for differentiated portfolio planning, evidence-based commercial strategy and increasingly complex product-level decision-making.

Value & Access

Value & Access remains one of the fastest-growing areas within the sector, accounting for 31% of mandates. This includes strategic and tactical market access capabilities across pricing and reimbursement, HEOR and RWE. Compared with last year, client demand has risen by 19%, reflecting the growing need to secure and sustain market access across global markets.

Analytics

Analytics roles remain steady with continued recognition of data-driven insights as a core enabler of strategic and operational decision-making. While demand is healthy, it also suggests headroom for future scaling as advanced analytics and AI become more deeply embedded in consulting solutions.

Supply Chain & Operations

Supply chain & operations mandates mark a significant shift within Life Sciences as organisations continue to prioritise resilience, digitalisation and end-to-end transformation. What was once viewed as a support functions have evolved into a specialised, business-critical capabilities as companies navigate global disruptions, cost pressures and increasingly complex product portfolios.

Our clients report increased demand for support, particularly across the areas of brand planning, customer engagement, omnichannel execution and post-launch optimisation.

Brand & Launch Strategy

Our clients report increased demand for support, particularly across the areas of brand planning, customer engagement, omnichannel execution and post-launch optimisation.

Sales

Sales-focused roles are still a need for businesses that are growing integrated account teams and business development functions to support broader service models and platform-based offerings. This aligns with the industry’s move toward more value-based engagements and more solution-led selling.

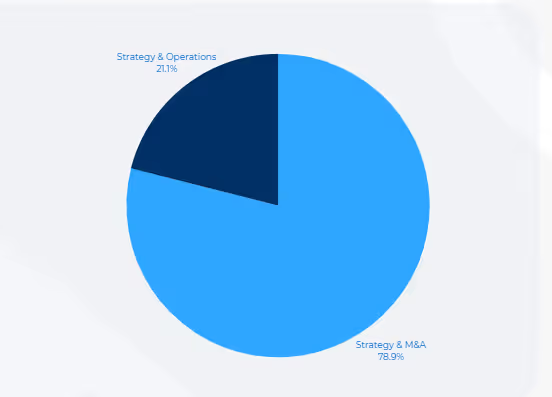

Hiring demand across core functional domains across all other industries

Strategy & M&A

Hiring demand in Strategy & M&A remains highly concentrated, with 67% of mandates centred on corporate & growth strategy and commercial due diligence. The remaining 33% of demand is distributed across wider private equity and M&A advisory services, including transaction support, post-merger integration, and exit readiness.

Strategy & Operations

Within Strategy & Operations, client demand has been evenly split: 50% of mandates were within procurement & supply chain, driven by ongoing cost-efficiency and resilience agendas, while the other 50% focus on transformation and operating model design, reflecting continued pressure on businesses to simplify, digitise, and scale effectively.

- Generalist - 23%

- Consumer & Retail - 19%

- TMT - 17%

- Private Equity - 15%

- Industrials - 8%

- Financial Services - 7.5%

- Healthcare - 7.5%

- Energy & Resources - 3%

Top five skillsets in-demand across all sectors in consulting

Commercial demand leads the market

Commercial roles continue to dominate the recruitment landscape, with over 35% of client requests focused on Corporate and Commercial Strategy talent. This reflects continued demand for expertise in growth strategy, deal support, and commercial due diligence. Within Life Sciences specifically, hiring has centred heavily on New Product Planning and Product Portfolio Strategy.

End-to-end capabilities

Mandates spanning strategic market access (pricing and reimbursement) and tactical market access (HEOR and value communications) remain resilient, particularly among organisations seeking partners that can integrate these capabilities with broader commercial strategy offerings.

Analytics continues to grow

Analytics signals continued expansion but still represents a measured level of investment – particularly within Life Sciences. Across other sectors, however, demand is accelerating for digital transformation and AI strategy capabilities.

Operations and supply chain momentum

This year has seen growing momentum across operations and supply chain roles, fuelled by client priorities around resilience, cost optimisation and delivery transformation. Demand for procurement and operational strategy talent is becoming increasingly central within generalist consulting, while Life Sciences specialists with supply chain expertise are rare to find but high in demand.

Future Outlook and Growth Plans in 2026...

- Within Life Sciences, Commercial Strategy & Access will remain central, while client demand continues to shift toward end-to-end, full-solution offerings for Biopharma.

- We anticipate continued growth in Analytics and AI as clients place greater emphasis on data-driven solutions, increasing demand for technically proficient, product- and platform-led talent (e.g. Product Managers) alongside strategy consultants who can translate insights into action.

- As clients pursue more integrated services and deeper partnerships in working across the full Biopharma product lifecycle, demand will continue to grow for talent across Operations, Supply Chain, Regulatory and Medical Affairs, Real-World Evidence (RWE), and Launch Execution.

- Across all areas, demand for experienced contractor and interim talent is rising and expected to continue into 2026. With KRS already supporting multiple workforce planning initiatives, consultancies are increasing contractor capacity to enable rapid access to high-calibre, flexible support for high-value engagements.

- Despite reduced M&A activity in the first half of the year, firms focused on M&A or private equity strategy have adapted well by broadening their offerings into wider advisory work, including operational excellence, performance improvement, and supply chain and procurement transformation. With PE activity gaining momentum, consultancies that can deliver both top-line commercial impact and performance-led operational improvements will be strongly positioned heading into 2026.

- Across our generalist offering, there has been continued demand in the Strategy & Operations space, with a number of new clients seeking senior operational talent.

A note from Steve Robertson

“2026 represents a strong next phase of growth for KRS, with continued expansion in our core markets alongside entry into new functional areas and industries. As our clients evolve in parallel, the year ahead will create a wealth of new opportunities for both clients and candidates in the consulting industry.”

Ready to partner with a team that understands Consulting?

Reach out today to discuss how we can support your consulting needs.